By definition, an amortization schedule is a guide that outlines exactly how our monthly mortgage payments are being used. For example, if your monthly mortgage payment is $1000, which part of that $1000 is being applied to interest on your loan and which part is being applied to the principle of your loan. I like to first explain that mortgages are NOT the same as a simple interest loan. In a simple interest loan, each of the payments is broken down into the same amounts for principal and interest every month for the entire duration of the loan term. With mortgages, however, the interest is front-loaded meaning the first years of your loan, the payment will be mostly be applied towards interest and less towards principal. This trend flip-flops eventually during the loan term and you end the mortgage with the majority of your payment being applied to paying down the principle balance. The amortization schedule breaks down this monthly trend month-by-month. Amortization schedules can be helpful in deciding what interest rate is best or how do extra principle payments really affect your loan over the long run.

Building wealth using investment properties is a 3-fold process. You have your

1. Monthly cash flow

2. Annual appreciation

3. Paying down the mortgage

Appreciation is something that takes time to build, but while you’re waiting for that to materialize, why not make the best use of the rest of the process?

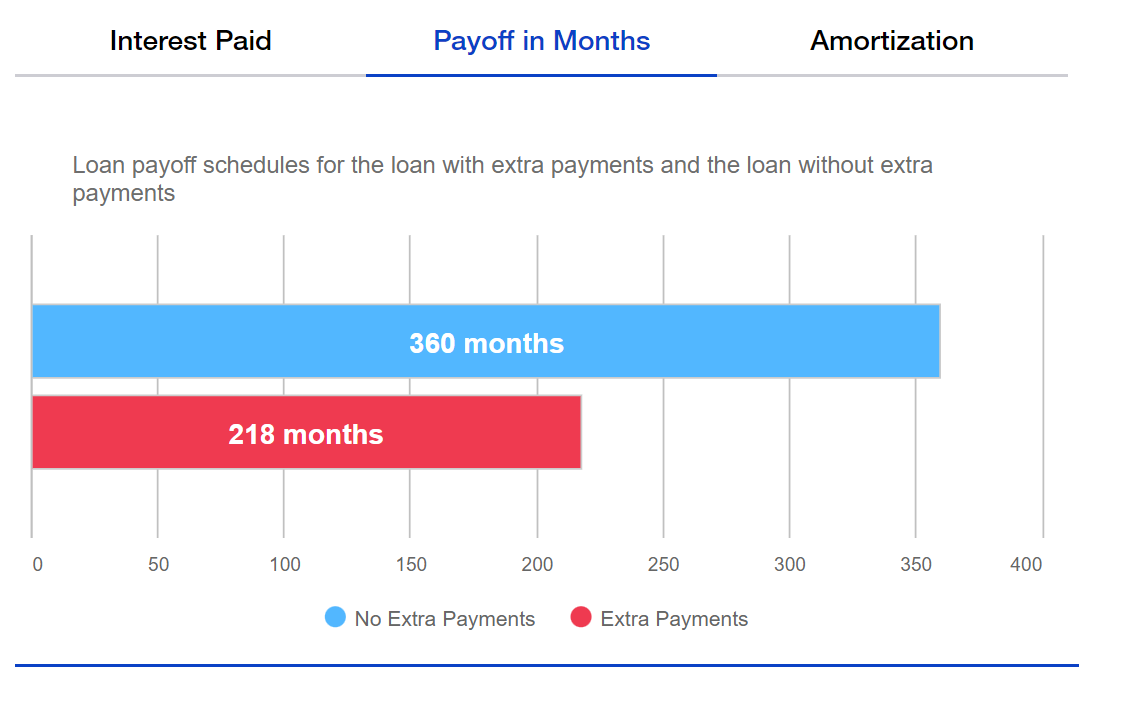

Extra Principal Payment Plan is the process of “over-paying” your monthly mortgage payment and allotting that overage to be applied directly to the principal balance. The theory behind this is the less principal balance you have, the less interest you’re paying on it. Such a simple idea, yet hardly anyone does this. Even a little bit can go a long way utilizing this method. Let’s look at the following example:

Example:

$200,000 loan amount at 6.0% interest rate with $100/mo. cash flow

If you take that $100/mo. cash flow and put it towards extra principal payments on that same loan, see below how the numbers change. Note: Your property will still break even and not cost you anything out-of-pocket per month to accomplish this.

Take notice on how the EPP changes things…

- Lowers your loan term by 65 months. That’s almost 5.5 years!

- Because your loan is paid off early, this gives you almost 5.5 years of free and clear income with no mortgage to consider. If your rent is approximately $2,000/mo., this provides around $116,000 income ($2,000 minus taxes and insurance estimates)

- Lowers the total interest paid by $49,138

All these benefits can be realized just for re-investing the $100 cashflow you would have probably spent on Starbucks or a dinner out. It’s something small you can do every month or whenever your budget allows that has a large benefit in the long run. Just keep in mind that the sooner the balance is paid off, the greater the impact!