Leveraging Equity in Your Investment Property: 1031 Exchange vs. HELOC

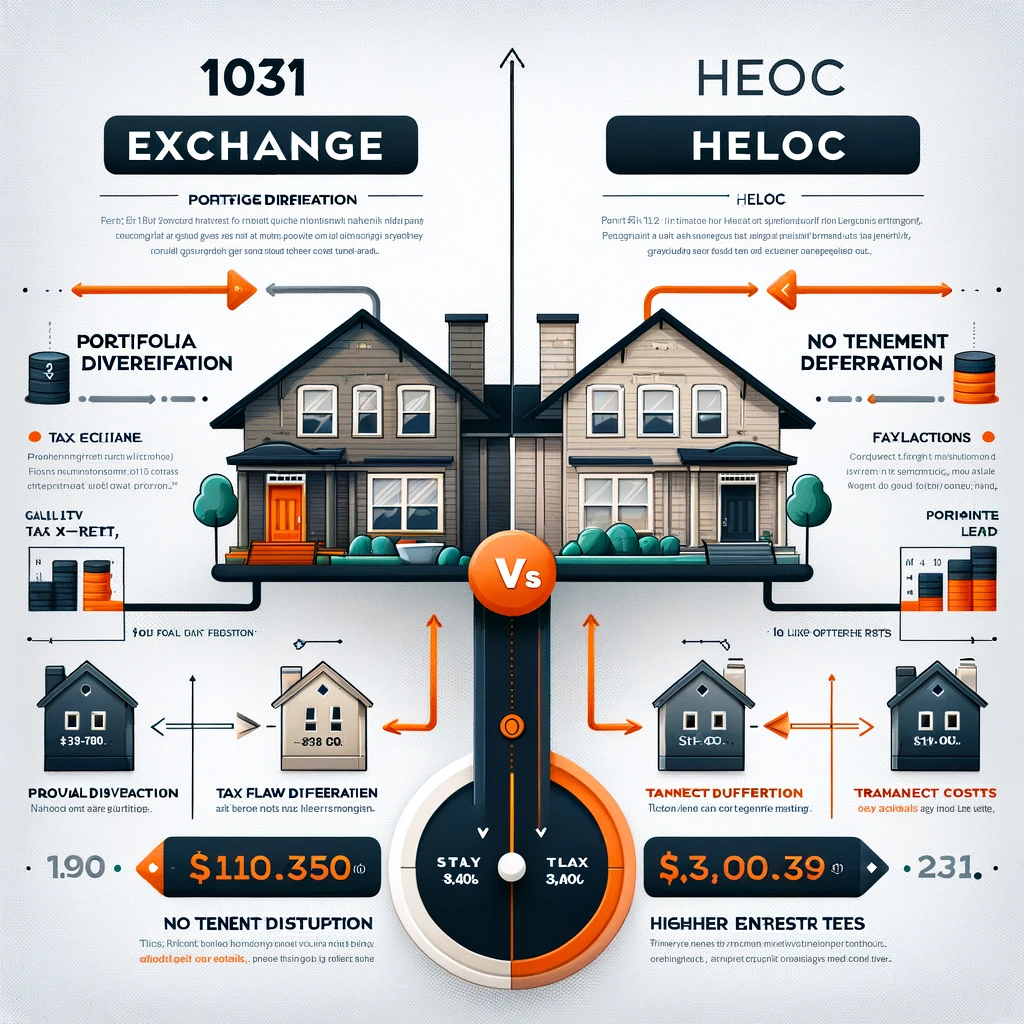

As a real estate investor, one of your greatest assets is the equity built into your properties. Tapping into this equity can be a powerful strategy for growing your portfolio...

As a real estate investor, one of your greatest assets is the equity built into your properties. Tapping into this equity can be a powerful strategy for growing your portfolio...

For investors, understanding the concept of points in mortgages can be tricky. It's often challenging to decide whether it's worth buying points or not.But what if I told you there's...

First, instead of explaining let's use an example. Let's say a buyer purchase a house 2 years ago for $200,000 and put $20,000 downpayment and took a mortgage of $170,000.Now let's...

Every year Atlas Van Lines shares with us migration patterns happening in the United States for the past calendar year. We've been tracking those migration patterns for several years and...

When homes sell in minutes and offers accept way over list price, how do you stand a chance?In recent months, I have seen a significant increase in our investors'...

We have found this great simple to under stand piece about real estate trends and bubble and where are we today with respect to the next bubble or bust. Read full article on...

As investors, we always want to get an edge, a better start, when we are buying an investment property.In today's market, it is hard to do.Yes, there are several ways...

Join us at Simple Real Estate Investing for Any Lifestyle on May 5th and 6th in Irvine!Investing in residential real estate is an excellent way to build your finances and save...

For as little as $30,000 you can buy yourself a nice investment property in a good area. So what does it look like in real life? For example: Purchase price: $130,000 Down-payment(20%): $26,000 Closing and...

Moving Trends: 2015 Annual Relocation Data Survey by MyMovingReviews....