EVERYONE WOKE UP! When we started talking about TAX REDUCTION through Real Estate.

Recently, I spoke to a real estate group in Redmond, WA. They looked tired. Weekend approaching, long week behind them, and honestly, maybe the lecturer (me) wasn’t the most exciting.

Then someone asked about taxes.

Suddenly, everyone woke up.

The question: “How can real estate reduce your tax burden?”

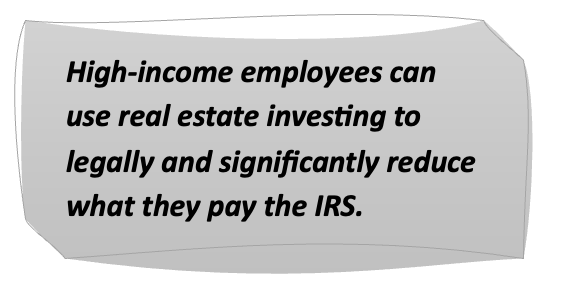

Here’s what got their attention: High-income employees can use real estate investing to legally and significantly reduce what they pay the IRS.

Read that again.

I’m talking real, meaningful tax reduction using strategies the tax code literally encourages.

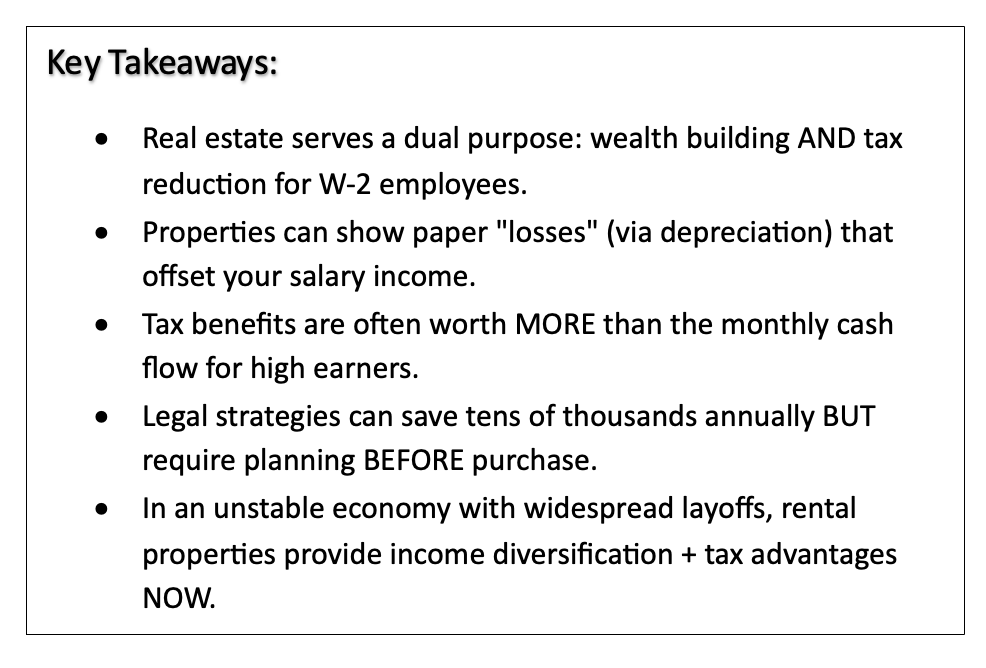

What Most Don’t Realize is that Real Estate Serves Two Purposes:Building Wealth (the obvious part) Tax Engineering (the part nobody talks about)

Even modest cashflow properties can generate substantial tax benefits, sometimes worth MORE than the monthly rent check itself.

➡️ That’s when the room really leaned in.

Over the last two years, I’ve been showing clients how real estate investing can leverage itself for tax planning in ways they never imagined when they started. Even if the investment doesn’t generate high cashflow, it can still help significantly reduce income taxes.

And if you’re a high-earner paying significant taxes while watching layoffs around you, this matters NOW.

Your Rental Property Can: Generate passive income streams Reduce your current tax burden Build long-term equity Create financial stability

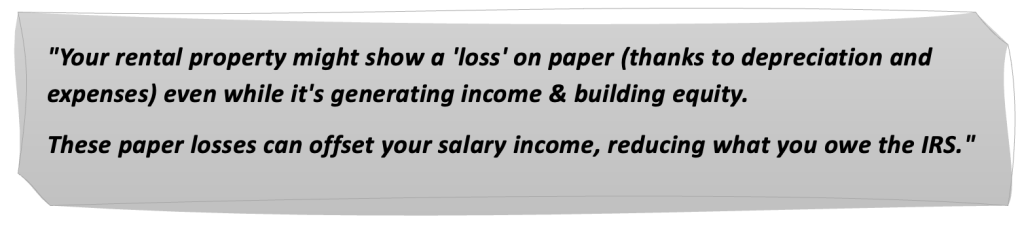

Did You Also Know: Your rental property might show a “loss” on paper (thanks to depreciation and expenses) even while it’s generating income and building equity. For high-income W-2 employees who qualify, these paper losses can offset your salary income, reducing what you owe the IRS.

There are multiple strategies your CPA can help you implement depending on your situation. The key is proper planning before you buy, not trying to retrofit tax benefits after.

Not every situation qualifies. Not every investor can use every strategy. But many situations do allow for these moves, and the savings can be substantial. We’re talking tens of thousands annually for high earners.

Important Disclaimer: I’m not a tax professional. This isn’t tax advice. Every situation is different, and you need to work with a qualified CPA who understands real estate tax strategies.

But what I can tell you is this: The U.S. tax code is designed to incentivize real estate investment. If you’re paying significant taxes and not taking advantage of these legal strategies, you’re leaving money on the table.

And right now, with employment uncertainty in tech and other industries, that money could be the difference between financial stress and financial security.

Let’s Talk Strategy

Watch the full video explaining this concept.Listening the a short podcast explaining this concept.

The Challenge:

Example:

-

Purchase Price: 10 years ago, you bought a house for $1 million as your primary residence.

-

Current Value: Today, it’s worth $3.25 million.

-

Net Proceeds After Sale: If you sell, you might walk away with $3 million after fees and costs (minus your mortgage balance)

Solution:

-

Convert Your Home to a Rental Property Move out of your home and rent it out (yes, for real OR pay $150,000+++ in taxes) Based on guidance from 1031 exchange experts, you typically need to rent it for at least one year to demonstrate that it has become an investment property. (Always confirm this timeframe with a qualified expert.)

-

Sell the Property as a Rental Once it’s classified as a rental, you can sell the property and use the proceeds in a 1031 exchange to buy new investment properties.

-

Utilize the Homeowner Tax Exemption As a primary residence, you’re eligible for a capital gains exclusion:$250,000 per individual $500,000 for a couple This means, in our example, that $500,000 of your gain is exempt from taxes.

-

Exchange the Remaining Equity The remaining $2.5 million (after the $500,000 exemption) becomes the “exchange amount.” You reinvest this into like-kind properties (e.g., rental properties) and defer taxes on that amount.

Tax Savings Example:

-

Without a 1031 exchange, you could face capital gains taxes on the entire $3 million gain.

-

By using the homeowner exemption and a 1031 exchange, you defer taxes on $2.5 million and pocket $500,000 tax-free.