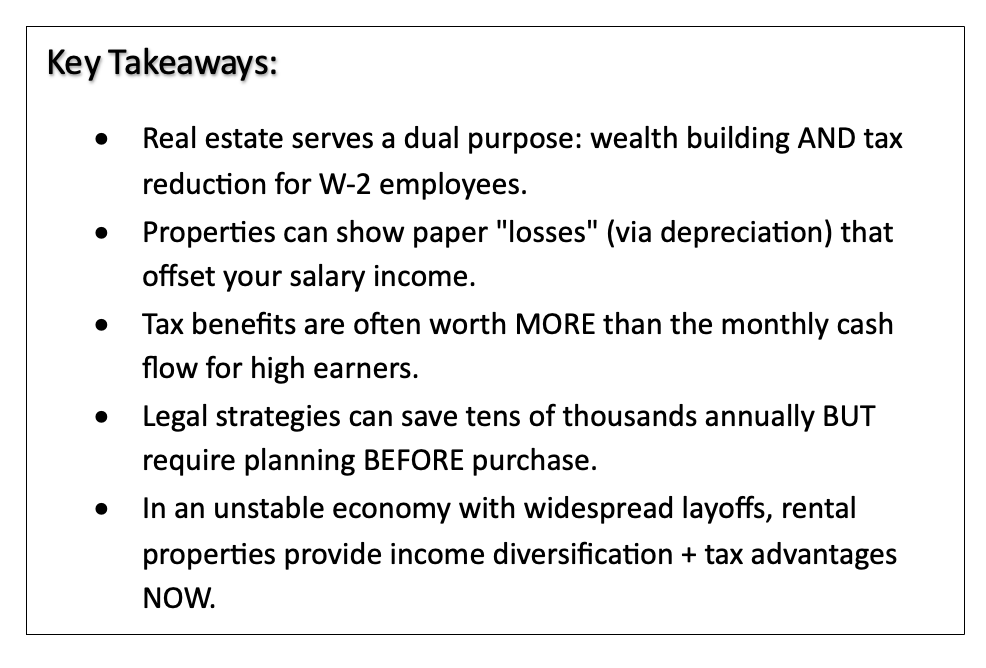

EVERYONE WOKE UP! When we started talking about TAX REDUCTION through Real Estate.

Recently, I spoke to a real estate group in Redmond, WA. They looked tired. Weekend approaching, long week behind them, and honestly, maybe the lecturer (me) wasn’t the most exciting.

Then someone asked about taxes.

Suddenly, everyone woke up.

The question: “How can real estate reduce your tax burden?”

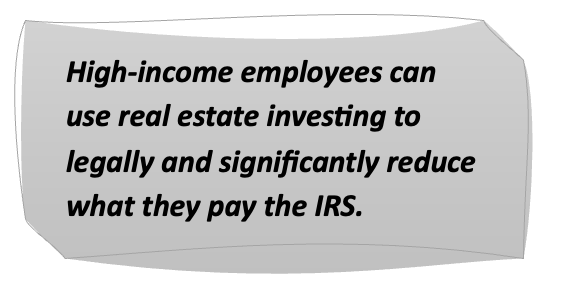

Here’s what got their attention: High-income employees can use real estate investing to legally and significantly reduce what they pay the IRS.

Read that again.

I’m talking real, meaningful tax reduction using strategies the tax code literally encourages.

What Most Don’t Realize is that Real Estate Serves Two Purposes:Building Wealth (the obvious part) Tax Engineering (the part nobody talks about)

Even modest cashflow properties can generate substantial tax benefits, sometimes worth MORE than the monthly rent check itself.

➡️ That’s when the room really leaned in.

Over the last two years, I’ve been showing clients how real estate investing can leverage itself for tax planning in ways they never imagined when they started. Even if the investment doesn’t generate high cashflow, it can still help significantly reduce income taxes.

And if you’re a high-earner paying significant taxes while watching layoffs around you, this matters NOW.

Your Rental Property Can: Generate passive income streams Reduce your current tax burden Build long-term equity Create financial stability

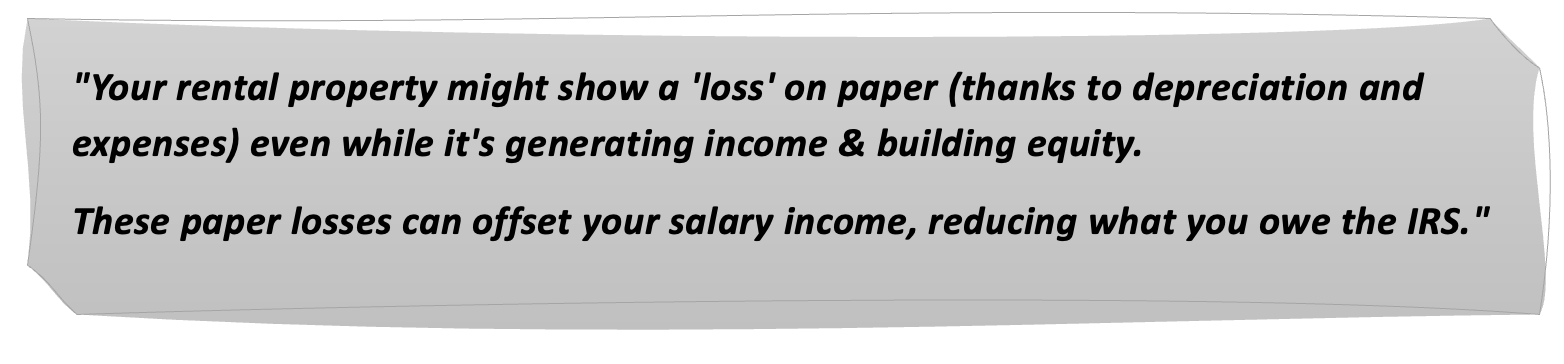

Did You Also Know: Your rental property might show a “loss” on paper (thanks to depreciation and expenses) even while it’s generating income and building equity. For high-income W-2 employees who qualify, these paper losses can offset your salary income, reducing what you owe the IRS.

There are multiple strategies your CPA can help you implement depending on your situation. The key is proper planning before you buy, not trying to retrofit tax benefits after.

Not every situation qualifies. Not every investor can use every strategy. But many situations do allow for these moves, and the savings can be substantial. We’re talking tens of thousands annually for high earners.

Important Disclaimer: I’m not a tax professional. This isn’t tax advice. Every situation is different, and you need to work with a qualified CPA who understands real estate tax strategies.

But what I can tell you is this: The U.S. tax code is designed to incentivize real estate investment. If you’re paying significant taxes and not taking advantage of these legal strategies, you’re leaving money on the table.

And right now, with employment uncertainty in tech and other industries, that money could be the difference between financial stress and financial security.

Let’s Talk Strategy

Watch the video about this topic:

https://www.youtube.com/@simplydoit1

📚 What This Post Is About:

- Understanding what a “Subject-To” real estate deal is

- Real-life example from investor Dani Beit-Or

- Pros, cons, and risks of this advanced investing strategy

- Why it could be a great opportunity in today’s market

⏱ Estimated Reading Time: 6 minutes

🔑 Highlights – Main Takeaways:

- A Subject-To Deal lets you take over a seller’s mortgage without getting a new loan

- Huge benefits include lower interest rates, built-in equity, and better cash flow

- Risks exist, like the bank calling the loan due, but these are rare and manageable

- These deals often require less upfront cost and no appraisal

- Dani shares how he successfully executed this strategy with real results

🏠 What Is a “Subject-To” Deal?

In this recorded session, I break down a creative and often misunderstood investing method: the Subject-To deal.

“Subject-To” (short for “subject to the existing mortgage”) means that instead of getting a new loan, you take over the existing mortgage payments from the seller. The mortgage stays in the seller’s name, but ownership of the property transfers to you (or your entity).

In this session, I explains how I personally used this strategy to:

- Lock in a 3.25% interest rate (compared to today’s 6.75%)

- Buy the property below market value, instantly gaining $55K–$60K in equity

- Avoid typical loan fees, appraisals, or mortgage approval delays

- Keep the mortgage off my credit report, protecting his DTI (Debt-to-Income ratio)

💡 Why Consider It?

- Built-in equity: I paid significantly less than market value, giving equity from day one.

- Better cash flow: Thanks to the low-interest mortgage, monthly income is higher.

- No credit impact: The loan doesn’t appear on your personal credit.

- Lower closing costs: Since you’re not getting a new loan, many of the typical lender fees are avoided.

- Faster to close: You skip many traditional hurdles.

⚠️ What Are the Risks?

Full transparency, there are challenges:

- “Due on sale” clause: Most mortgages have this, which gives the bank the right to demand full repayment if the title changes hands. However, in over 20 years, I’ve only seen this happen twice—making it a low-probability but real risk.

- Seller cooperation: You need the seller to sign multiple documents and stay responsive during the process.

- Insurance complexities: You may run into hurdles when trying to change or update the insurance policy if it’s still in the seller’s name.

- Document-heavy: These deals require 10+ legal and notarized documents, especially for things like permission to speak with the lender, county, insurance, etc.

🧠 How to Approach It

- Go in with eyes open: Know the risks, but also understand how rare some of them are.

- Mitigate risk with equity: If you’re getting significant equity on day one, you have room to refinance or sell if needed.

- Lean on experience and support: This strategy isn’t for beginners, but it can be powerful when done with the right knowledge and team.

💬 Final Thoughts

This approach, though more advanced can unlock deals that would otherwise seem impossible. It’s not about cutting corners but finding smarter ways to invest in the current market.

Creative financing isn’t just theory. It’s working! And it could work for you too if done right.